7 Critical Parts of Every Real Estate Investment Business Plan

7 Critical Parts of Every Real Estate Investment Business Plan

Do you like this Article ?

Sign up HERE for your FREE M&M Account to receive more Real Estate related information and news and THIS article.

M&M Membership includes: FREE Coaching Events & Workshops, access to our Real Estate News Group (Local & National Real Estate and Financial News), access to social media marketing tips and nuggets, So Cal weekly market report, and much more.

7 Critical Parts of Every Real Estate Investment Business Plan

Buying your first investment property is an incredible thrill, but whether you want to fix and flip or buy and hold, you need to have a solid real estate investment business plan.

In this article, we’ll discuss the common requirements of any business plan, such as budget and financial projections, as well as required capital. We will also review less common, yet equally important, items like investment strategies, market analysis, property acquisition, and time commitment.

Parts to a Real Estate Investment Business Plan

- Investment Strategy

- Market Analysis

- Property Acquisition

- Time Commitment

- Budget and Financial Projections

- Funding Requirements

- Exit Strate

Investment Strategy

Whether it’s a cash-flow, short-term rental, fix and flip, speculation, or wholesale, your real estate investment business plan should begin with the strategy that you wish to pursue.

Each investment strategy poses its own benefits and risks. Upfront investment, time commitments, return, and difficulty should all be considered when you are selecting your real estate investment strategy.

Reviewing the chart above, you can see that cash-flow investing is a great option if you are looking for an easier strategy that will allow you to retire in 20 years by owning properties that are free and clear. However, cash-flow investing may not be the best strategy if you want to generate immediate income or you wish to make real estate investing a full-time career.

Wholesale real estate investing is a good choice if you’re looking for short-term opportunities to break into the investing industry by leveraging your existing skills as an agent. Short-term rentals and fix-and-flip projects are much more labor-intensive, but they’ll both pay off much sooner than speculative deals.

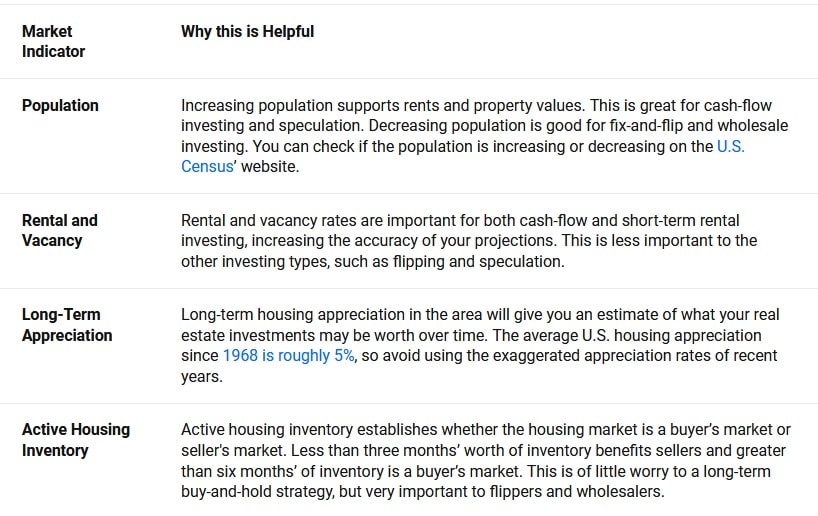

Market Analysis

The next part of your real estate investment plan is to determine the location or locations you would like to invest in. Then you must determine if the market conditions in those locations are right for your strategy. One of the biggest mistakes real estate investors make is using a strategy that doesn’t fit with the market conditions or area.

Success in real estate investing is less often dependent upon the skills or talent of the investor and more often the timing of the market. The saying “a rising tide floats all boats” comes to mind. The following market indicators can give you insight on the direction the real estate market is going.

Property Acquisition

As a real estate professional, you are likely presented with investment opportunities every day. What’s different about becoming a serious real estate investor is having a business plan that demonstrates how you will identify, vet, and acquire properties. Therefore, your business plan should reflect how you plan to identify, vet, and acquire properties.

Many novice investors think they can just contact a local agent and select from the properties that are available in the MLS. The cold truth is that the best deals are found off-market or outside of the MLS. This means that you may need to create a plan for marketing to homeowners in foreclosure or divorce and bankruptcy attorneys.

Once you have a steady stream of investment opportunities coming your way, you will also need a process for quickly evaluating whether each property fits your investment strategy. Fortunately, we have created guides to help you analyze both fix-and-flip and cash-flow real estate investments.

Time Commitment

Another consideration for a real estate investment business plan is the time you have available to contribute to investing. Each of the investment strategies above will require some time commitment from you. If you are limited on time, you may need to hire someone to manage your investments.

If you are doing fix and flips and have a lot of free time to manage contractors, then you may be the best person to manage the project. However, if you are buying a cash-flow property in another state, it is nice to have a property manager in the area to find tenants, handle emergencies, and collect rents.

If you are planning on hiring people to help you with your investments, you will need to remember to add the associated costs to your budget and financial projections.

Budget and Financial Projections

The next part of your real estate investment business plan is to prepare an estimate of the fixed and variable expenses you may encounter from your investment activities, as well as a projection of potential revenues.

Expenses

When estimating expenses, make sure to include expenses related to the property—such as taxes and utilities—and expenses that are related to managing a real estate investment business, like employees, software, and property management services.

Revenue

Then, estimate your revenue. Revenues will be very different depending on the type of investing strategy you are using. If you are a wholesale investor, you may buy and resell multiple properties throughout the year, producing substantial revenue. If you are cash-flow investing, you will have consistent revenues from the rental income. And speculative land investing may not produce any revenue until it is sold—and that may take years!

Financial Projection

When you combine your expenses and revenue projections, you will be able to estimate your financial projection. The financial projection is a five- to 30-year estimate of your budget that will also take into consideration other important items such as appreciation, principal reduction, and depreciation.

The overall goal with your budget and financial projections is to accurately estimate the capital and funding needed to execute your real estate investment business plan.

Funding Requirement

Funding requirements are a combination of the cash, financing, hard money or private financing you will need to execute your real estate investment business plan. Once you complete your financial projections, you can easily estimate the total investment needed.

A great benefit of real estate investing over other types of investing is the ability to leverage. In many cases you can finance 60% to 80% of the acquisition price, and some hard money lenders will finance the repairs too.

In either case, you want to ensure you have plenty of money on hand to weather the ups and downs until you are ready to exit. Most business plans estimate an additional cash-on-hand figure of 20% of the agreed-upon purchase price.

Exit Strategy

Any good real estate investment business plan includes an exit strategy. Sure, you may say that you are going to hold your properties forever, but the truth is, you still need to have the ability to exit if your plans change.

An exit strategy is not a requirement to sell; it is the point in your investment plan that allows you the option to exit if you decide to. Experienced investors know that you can only really control when you buy; due to unforeseen circumstances, you can’t always control when you must sell.

To identify your exit strategy, review your financial projections and identify points where your balance sheet reflects low liabilities alongside high cash and equity. These are good exit points. For fix and flips and wholesale, the exit strategy may be months or even weeks for each property; for speculation and cash-flow it may take five to 10 years.

The Bottom Line

Real estate investing can be fun and very profitable. To ensure your success with real estate investing, start with a well-thought-out plan. As they say: “Failing to plan is planning to fail!”

If you have great real estate investment advice, please share in the comments below.

Source: www.theclose.com

Author: Sean Moudry

M&M NEWS

Related Articles

The Real Estate Market is Cyclical, Don’t Panic, Adjust!

The Real Estate Market is Cyclical, Don’t Panic, Adjust! The Real Estate market is cyclical. The data shows, and it’s clear that we are experiencing one of the toughest real estate markets in the past decade. As bad as it is, there are certain agents who do well,...

Why the housing market is going from tough to terrible

Why the housing market is going from tough to terrible Do you like this Article ? Sign up HERE for your FREE M&M Account to receive more Real Estate related information and news and THIS article. M&M Membership includes: FREE Coaching Events & Workshops,...

As mortgage rates hit 8%, home ‘affordability is incredibly difficult,’ economist says

As mortgage rates hit 8%, home ‘affordability is incredibly difficult,’ economist says Do you like this Article ? Sign up HERE for your FREE M&M Account to receive more Real Estate related information and news and THIS article. M&M Membership includes: FREE...