Mortgage Interest Rates Forecast: How High Will Rates Climb In 2022?

Mortgage Interest Rates Forecast: How High Will Rates Climb In 2022?

Natalie Campisi

Mortgage Interest Rates Forecast: How High Will Rates Climb In 2022?

The cost of lending is rising as mortgage rates continue to shoot up—and that will impact the bottom lines of homeowners and borrowers alike. The average fixed rate on a 30-year mortgage reached 5.27% in early May, the highest level in more than a decade. So folks who are hoping for rates to fall may be waiting for a while.

Rising inflation is one reason we can expect rates to climb. In March, the consumer price index (CPI) rose to 8.5%, its highest level since 1981. Another catalyst was the Federal Reserve raising its rate by 50 basis points in May, the biggest increase in more than two decades.

“Aggressive inflation will force the Federal Reserve to raise interest rates multiple rounds this year and actively pursue quantitative tightening,” says Lawrence Yun, chief economist and senior vice president of research at the National Association of Realtors (NAR). “That is why mortgage rates recently have shot up so high. Higher mortgage rates will inevitably pull home sales down in the coming months and slow home price appreciation.”

Related: Compare Current Mortgage Rates

Mortgage Rates Forecast for May 2022

Rising inflation and the Fed’s monetary policy are all putting pressure on mortgage rates. As inflation increases, the Fed reacts by applying more aggressive monetary policy, which invariably leads to higher mortgage rates.

“The pressure to contain inflation will grow and the Fed will have to raise its fed funds rate eight to 10 times with quarter-point hikes this year,” says Yun. “Additionally, the Fed will undo the quantitative easing steadily, which will put upward pressure on long-term mortgage rates.”

Mortgage rates are directly impacted by U.S. Treasury bond yields but actions by the Fed and economic factors can influence rates.

Experts are forecasting that the 30-year, fixed-mortgage rate will vary from 4.8% to 5.5% by the end of 2022. Here’s their more detailed predictions, as of mid-April 2022:

- Mortgage Bankers Association (MBA): “Mortgage rates are expected to end 2022 at 4.8%–and to decline gradually to 4.6%–by 2024 as spreads narrow.”

- NAR’s Yun: “All in all, the 30-year fixed mortgage rate is likely to hit 5.3% to 5.5% by the end of the year. Some consumers may opt for a 5-year ARM (adjustable-rate mortgage) at 4% by the end of the year.”

- Matthew Speakman, senior economist at Zillow: “Competing dynamics suggest that there will be little reason for mortgage rates to decline anytime soon.”

Is There Still Time To Refinance?

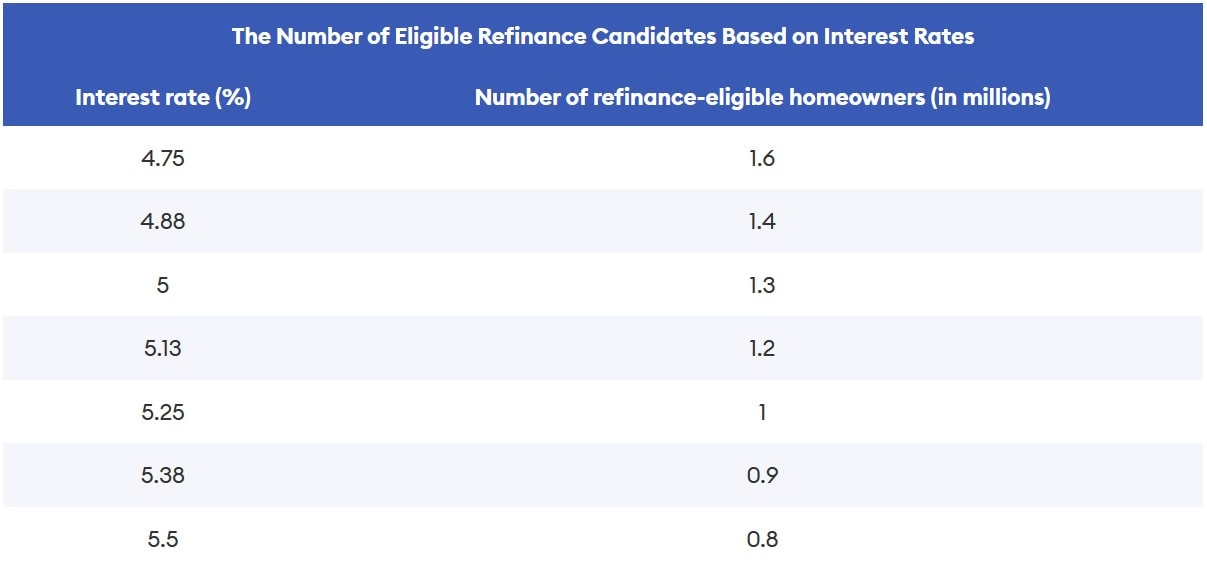

With mortgage rates quickly rising, homeowners are racing to save money on refinancing. Currently, the average rate on a 30-year fixed mortgage is hovering around 5%, where roughly 1.3 million borrowers are still eligible to refinance, according to Black Knight, a data analytics company. Each time rates inch up, fewer borrowers will be able to save money by refinancing.

Black Knight defines refinance-eligible borrowers as having a minimum of 720 credit scores, 20% equity in their home, and the ability to shave off at least 0.75% of their interest rate by refinancing into a 30-year fixed mortgage.

While refinancing options can lead to a lower monthly payment, not all of the options yield less interest over the life of the loan. For example, refinancing from a 5% mortgage with 26 years left on it to a 4% rate but at 30 years will cause you to pay more than $13,000 in interest.

Before you start shopping around for a lender, you can find out how much you could save by using a mortgage refinancing calculator.

You’ll also want to consider how long you plan on staying in your home as the closing costs can eat up your savings if you sell shortly after refinancing. The closing costs to refinance run between 2% to 5% of the loan amount depending on the lender. So you should plan on keeping your home long enough to cover those costs and realize the savings from refinancing at a lower rate.

Keep in mind, the rate you qualify for also depends on other factors such as your credit score, debt-to-income (DTI) ratio, loan-to-value ratio (LTV) and proof of steady income.

Current Mortgage Rate Trends

The average weekly mortgage rate for a 30-year fixed has jumped to 5.27% as of May 5, the highest level in 13 years.

The average cost of a 15-year, fixed-rate mortgage has also increased to 4.52% as of May 5, up 2.30 percentage points compared to a year ago.

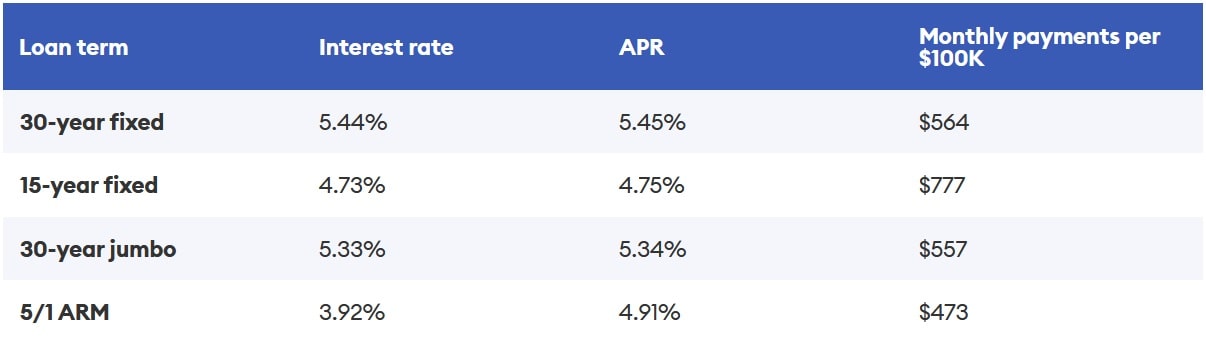

Current Mortgage Rates for May 2022

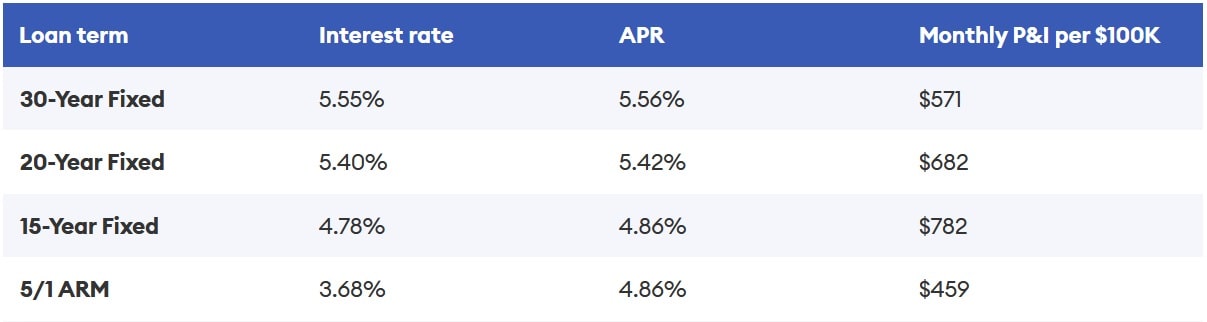

Current Refinance Rates

Source: forbes.com

M&M NEWS

Related Articles

The Real Estate Market is Cyclical, Don’t Panic, Adjust!

The Real Estate Market is Cyclical, Don’t Panic, Adjust! The Real Estate market is cyclical. The data shows, and it’s clear that we are experiencing one of the toughest real estate markets in the past decade. As bad as it is, there are certain agents who do well,...

Why the housing market is going from tough to terrible

Why the housing market is going from tough to terrible Do you like this Article ? Sign up HERE for your FREE M&M Account to receive more Real Estate related information and news and THIS article. M&M Membership includes: FREE Coaching Events & Workshops,...

As mortgage rates hit 8%, home ‘affordability is incredibly difficult,’ economist says

As mortgage rates hit 8%, home ‘affordability is incredibly difficult,’ economist says Do you like this Article ? Sign up HERE for your FREE M&M Account to receive more Real Estate related information and news and THIS article. M&M Membership includes: FREE...