Seller’s Market, Buyer’s Market, ‘Nobody’s Market’? The Weird State Of Housing Right Now

Seller’s Market, Buyer’s Market, ‘Nobody’s Market’? The Weird State Of Housing Right Now

Do you like this Article ?

Sign up HERE for your FREE M&M Account to receive more Real Estate related information and news and THIS article.

M&M Membership includes: FREE Coaching Events & Workshops, access to our Real Estate News Group (Local & National Real Estate and Financial News), access to social media marketing tips and nuggets, So Cal weekly market report, and much more.

Seller’s Market, Buyer’s Market, ‘Nobody’s Market’? The Weird State Of Housing Right Now

Today’s housing market has everyone wondering: Is it still a seller’s market, or has the power dynamic finally shifted in favor of buyers?

Try neither.

Uncertainty about the future of inflation, the economy, mortgage rates, and more have seized up the market—and wrenched power away from buyers and sellers alike.

“Today, real estate is ‘nobody’s market,’” notes Realtor.com® Chief Economist Danielle Hale in her analysis of housing data for the week ending Feb. 4. “The number of homeowners deciding to sell continues to lag, but inventory and time on market continue to climb, reflecting still-hesitant buyers.”

We’ll break down what the latest real estate statistics mean for homebuyers and sellers in this latest installment of “How’s the Housing Market This Week?”

Affordability on ‘the brink’

Although mortgage rates for a 30-year fixed-rate home loan have fallen from October’s 20-year high of 7.08%, they’re still high enough to leave a whole lot of buyers leery about closing the deal.

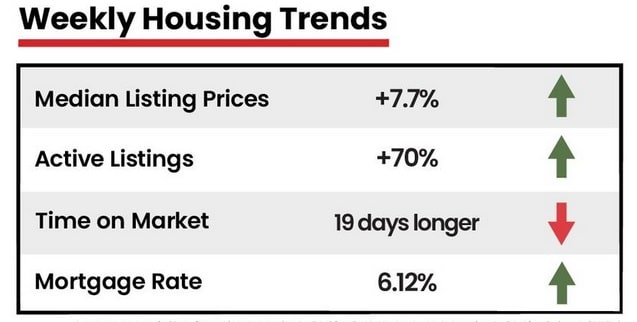

For the week ending Feb. 9, interest rates continued along their recent jagged path, ticking up to 6.12%, according to Freddie Mac.

Meanwhile, median listing prices, which hovered around $400,000 in January, are still higher than they were last year. For the week ending Feb. 4, prices were up 7.7% compared with this same week a year earlier.

“With high home prices and mortgage rates pushing affordability to the brink for many potential buyers, market activity and pricing will be more dependent than usual on the trajectory for mortgage rates,” says Hale.

More homes are sitting on the market

With home prices and mortgage rates still uncomfortably high, buyers just aren’t biting, leading to a glut of real estate listings gathering dust. For the week ending Feb. 4, home inventory shot up by 70% over levels seen this same week a year earlier.

As a result, many homeowners simply do not want to sell their homes as of late. New listings were down by 11% from one year ago for the week ending Feb. 4.

That marks 31 weeks that fewer sellers have put their homes on the market compared with last year, and for good reason: Sellers might not only struggle to sell, but if they succeed, many might have to face the same steep home prices and mortgage rates as other buyers, making it a lose-lose scenario all round.

“High costs and mortgage rates can significantly up the ante for homeowners hoping to trade up and remain in their current area,” explains Hale. Many are deciding to just stay put.

Plus, this continuing lull in new listings means homebuyers might not be all that excited by the idea of sifting through stale, steeply priced properties.

“With new listings declining, the growing number of homes for sale reflects still-low buyer interest amid high costs,” adds Hale.

Some good news for home shoppers

In January, homes lingered on the market for 75 days. And for the week ending Feb. 4, listings sat for 19 days longer compared with this time last year. Overall, the housing market is currently experiencing a 28-week trend of homes lingering on the market for longer periods than they did a year earlier.

But this presents a unique opportunity for buyers willing to comb through old listings for bargains.

“January data also reveals a significant increase in the share of homes for sale with a price reduction, more than double compared to the same period last year,” says Hale.

Slow movements in the market signal hope

Despite the morass many buyers and sellers find themselves in, there is evidence the market is trudging forward.

“Looking ahead, in addition to a slowing decline in existing-home sales in December, both new-home sales and pending home sales saw an uptick,” says Hale. “These indicators, which track early stages of transactions, jibe with the sentiment data that shows a very modest improvement.”

Buyers now have more time to carefully consider their options. And when they find a home, they can try striking a deal.

Sellers can take heart that despite inventory surging, January data shows that most housing markets have fewer homes for sale than were typically available pre-pandemic. If a seller has a good home that’s priced right, it will likely sell quickly.

“Longer time on market overall doesn’t necessarily mean longer time on market for the most desirable homes,” Hale explains.

So perhaps both buyers and sellers might shake hands on more deals soon enough.

Source: www.realtor.com

Author: Margaret Heidenry

M&M NEWS

Related Articles

The Real Estate Market is Cyclical, Don’t Panic, Adjust!

The Real Estate Market is Cyclical, Don’t Panic, Adjust! The Real Estate market is cyclical. The data shows, and it’s clear that we are experiencing one of the toughest real estate markets in the past decade. As bad as it is, there are certain agents who do well,...

Why the housing market is going from tough to terrible

Why the housing market is going from tough to terrible Do you like this Article ? Sign up HERE for your FREE M&M Account to receive more Real Estate related information and news and THIS article. M&M Membership includes: FREE Coaching Events & Workshops,...

As mortgage rates hit 8%, home ‘affordability is incredibly difficult,’ economist says

As mortgage rates hit 8%, home ‘affordability is incredibly difficult,’ economist says Do you like this Article ? Sign up HERE for your FREE M&M Account to receive more Real Estate related information and news and THIS article. M&M Membership includes: FREE...